March 2023: JPMorgan Chase doesn’t care about your deposits

TL:DR;

Chase, BofA, and Wells (and other large banks) aren’t for everyone

All deposits (not just G-SIB deposits) are effectively insured. That knowledge is emergent

Social media + online banking accelerate deposit flight. This makes banks more vulnerable to runs than ever before

Regulators must adjust their framework/toolkit to this new reality

Long before joining Cash App, I traded U.S. Treasuries at Bank of America. Back then, Chase was a formidable competitor to BofA in 2004, and a decade later Chase was a formidable competitor to Cash App. With all that said, Chase (and BaML, and Wells, and Citi) simply do not care about the marginal retail/SMB/startup company’s deposit. It’s one reason why the interest rates paid on savings are basically 0%; they are simply not competing for your deposits [4]

Chase (and the remainder of the US based Global Systemically Important Banks or G-SIBs) don’t need more retail or retail-ish (startup and true SMB) deposits, from anyone. They have more than enough access to liquidity via debt, preferred financing and term deposits, and they are incredibly well capitalized, partly due to their G-SIB status. Historically, banks tended to like sticky retail deposits, but maybe those models are wrong now that we just saw a $42bn twitter driven digital bank run occur.

Deposit flight is easier than ever

Corporate deposits have always been higher flight risk than retail; they’re more likely over the deposit insurance cap, corporate officers are liable to shareholders for mismanagement, and banks that focus on a narrow industry vertical can suffer from network effect issues (as SVB did). My hypothesis is - retail-ish (basically non corporate) deposits were believed to be sticky, but no longer are. In the old world there was an incredible amount of friction to deposit flight - each depositor would have to take time off from work or family, go to a branch or call in, wait in line, ask for their money, and then do something with that cash or cashier’s check once they had it. You saw this in how long it took for deposits to flee (eg Wachovia depositors took 19 days to withdraw $18.3bn in deposits) [1]

In today’s world, >99% of any bank’s deposits can be transferred to another bank in a single day, at any time of day, from a phone or computer. This is as true for GSIBs like JPM Chase, as it is for regional banks like SVB. The main difference between Chase and SVB is that prior to last week, Chase deposits were perceived as fully insured (over and above $250k deposit insurance cap), and SVBs were not. This doesn’t make deposit flight mechanically any harder for Chase - it just makes it less probable as depositor perception is that their deposits will be recovered at Chase no matter what. It’s likely that retail deposits are actually much less sticky regardless of which bank they reside in today than in the past, and the SVB collapse was a catalyst to spreading that insight. If the hypothesis is correct, then fractional reserve banking as practiced in the US today is in peril (because no bank, no matter how well capitalized, can survive 25% deposit flight in a 48h period).

Perception of insolvency = insolvency

My takeaway from Diamond-Dybvig is really that depositor expectations of other depositor behavior are sufficient for a bank run, regardless of whether the bank’s actually solvent. Which means all that’s needed for a bank run is for enough people to believe that other depositors are taking their money out (rather than actually not having enough assets to cover its liabilities on any time horizon). Being actually insolvent is necessary but not sufficient for a bank run. Being perceived as insolvent is necessary and sufficient for a bank run. In hindsight this has always been true[3], but the differences today are

Social media in its current incarnation has accelerated the rate at which a belief can spread. This means depositor sentiment about a bank can turn negative in a day, which is faster than even the best prepared regulator can respond

Depositors can withdraw deposits much more quickly than before (there’s no longer a physical constraint to every depositor going online to initiate an ACH withdrawal at the same moment)

To put this in context - almost as much deposits left SVB ($42bn) in 2 days than the bank’s peak equity market capitalization (~$43bn).

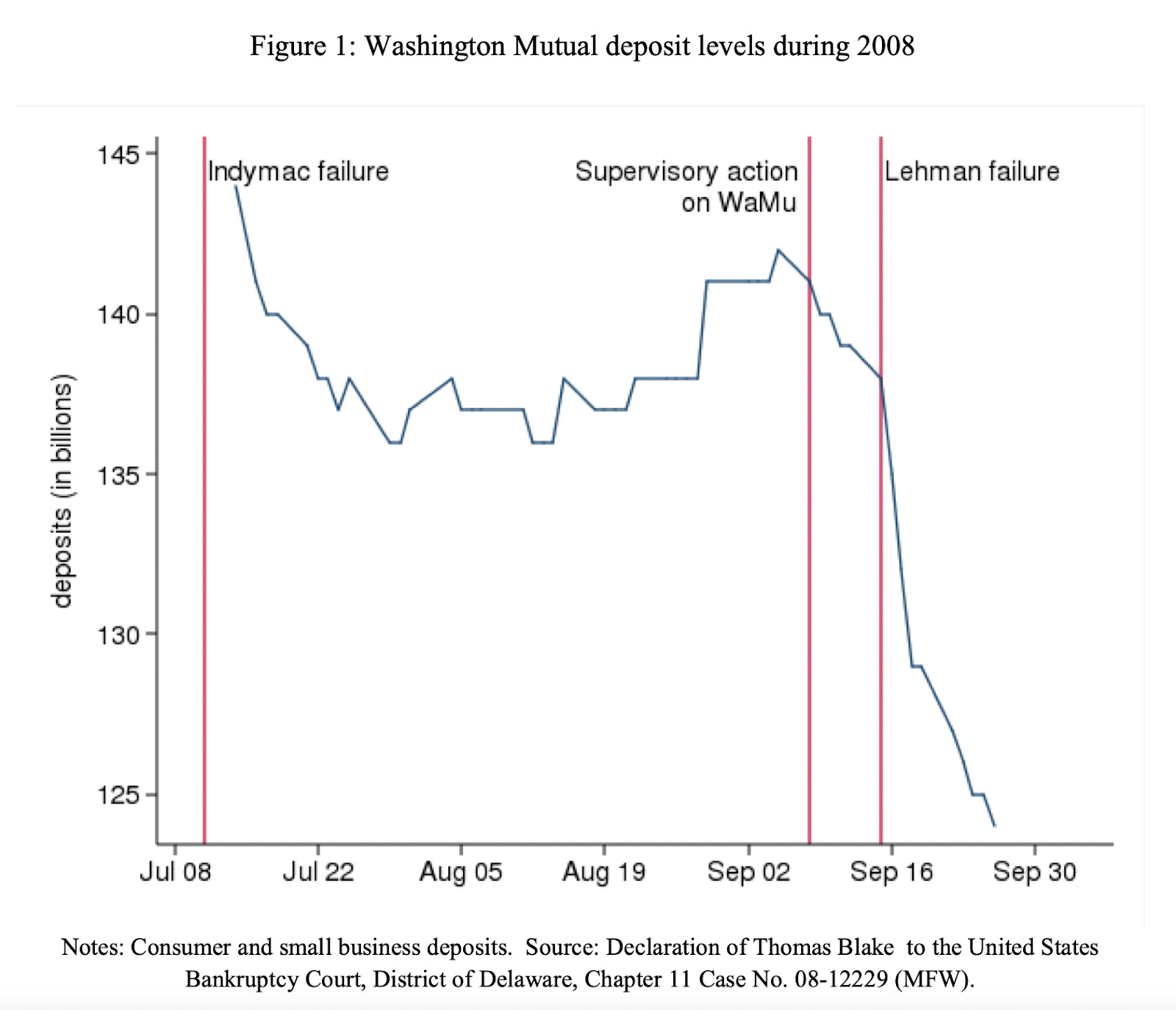

For scale, $42bn in deposit outflows represents 25% of SVB's 2022 deposit base gone in 48 hours. Wachovia experienced $18.3bn in deposit outflows over 19 days in September 2008. Even Washington Mutual which was the 6th largest depository institution at the time, peak to trough in September 2008 experienced only $20bn in deposit outflows over 3 weeks or so, just north of 11% of it's deposit base of $145bn. [1]

What took Washington Mutual depositors 3 weeks to do, SVB depositors did in 24 hours. Bank runs are happening faster, and cutting deeper than ever before.

Regional banks serve customers that Chase doesn’t want

SVB existed (exists?) for a reason (and regional banks exist for a variant of this reason) - they serve a customer segment that Chase and other G-SIBs do not care about, and they take risks that Chase won’t, that by definition take a long time to see to fruition. Not every loan can be securitized, and a well functioning economy needs a way to fund long term investment. This isn’t a knock on Chase - you can’t be all things to everybody, and the customer Chase cares about is a giant company with lots of financial complexity, consuming investment banking products, debt capital markets, issuing etc, not a subscale startup trying to buy money market funds. Chase is not going to be offering anyone venture debt - it just doesn’t matter enough to move the needle for them.

In the wake of the SVB bank run, many VC and PE funds instructed their portfolio companies to move permanently off regional banks. This isn’t isolated - G-SIBs have been inundated [2] with requests for new account openings, and a lot of these investors and startups are about to discover why people banked with SVB in the first place. I suspect a lot of startups are having this experience right now:

And it’s not just account opening - even things like freezing a new account when a large unexpected wire comes in is fairly commonplace for large bank risk systems. For startups however, that’s just a fundraise.

At a high level, if you’re the CFO of a company with $6m in deposits, no one at Chase is picking up your call, but the banker at SVB (or your regional bank of choice) was. You might think this applies only to startups, but there are a LOT of entities in America at that stage. Its the reason an opening for Square Bank existed, it’s the reason Stripe Capital exists, and it’s the reason 4000 regional banks and credit unions exist. The long tail is a lot longer than you think.

For full disclosure, I’m an investor in Mercury, and I think they’re great and stuff, but the thing that gave me the conviction that they would work, was this; In 2017 I had to open a business checking account, and I tried to do it with Chase. I had to go into a Chase branch and talk to someone. After that, I had to call twice with additional details, and send two faxes over the course of 3 weeks, after which the account wasn’t open. Again, this doesn’t mean Chase is bad. It just means a) I’m not the customer Chase is targeting, and b) if you’re reading this, you’re probably not either.

Post ZIRP, all deposits are effectively insured

All deposits are effectively insured; this was implicitly true before March 2023, it just took the SVB collapse for us all (including the regulators) to realize it. If enough of the public perceives their deposits to be insured, then the deposits effectively are (because that perception creates sufficient political gravity that regulators can’t ignore it). Post 2008, G-SIB deposits are perceived by the public as insured (which explains why deposit flight moved from SVB to G-SIBs, not from SVB to other regional banks). Now all deposits at all banks are effectively insured, because the public perception is that regulators will not allow them to lose any deposits. After all, if I as a consumer or small business have to be smart about the soundness and safety of a specific bank before putting my money in it, whats the point of having a regulator in the first place?

Regulators simultaneously have to adapt to this new perception by the public, and develop tools to respond to the reality that 1) depositor sentiment can now collapse in a day, and 2) all deposits can now be liquidated in a day.

I don’t think this fact is fully priced in; technically deposits are only insured up to $250k per depositor per institution, but perceptively all deposits are safe at any bank in the US. The day this isn’t true (ie the day depositors lose deposits in a bank failure) 99% of deposits will flow to the bank that’s perceived to be the safest, which will most likely be a GSIB. That’s what was happening in the SVB collapse prior to regulatory intervention, and that’s the future waiting in the wings for the next bank failure.

Thanks to Temi Omojola and Brandon Carl for reading this in draft form

[1] https://www.federalreserve.gov/econresdata/feds/2015/files/2015111pap.pdf

[2] https://www.ft.com/content/2b580939-a4b6-48d2-8eb6-629b4cb1e06c

[3] http://minneapolisfed.org/research/QR/QR2412.pdf

[4]

Great write up today, Ayo. On point as usual.